With changes to capital gains tax, new minimum tax rates and the restrictions on negative gearing either commenced or on the horizon you might be forgiven for thinking that all the recent tax news is about paying more.

But the end of the financial year is also a time to think about how you can get some of that tax repaid to you.

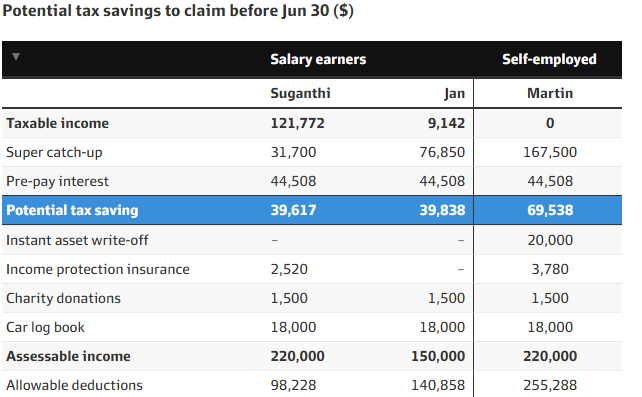

To demonstrate the powerful effect that claiming legitimately incurred, and documented, expenses can have, we look at five key deduction types.

We will use hypothetical taxpayers Suganthi, Martin and Jan to explain how it works in practice. Suganthi earns a salary of $220,000, Martin is self-employed and earns the same amount and Jan has a wage of $150,000.

In the unlikely event that they each used all five deductions, Suganthi could obtain a tax refund of almost $40,000, and Martin and Jan could end up with no tax to pay.

Before we explain each deduction, it’s important to note that we aren’t talking about free money – you only get a refund if you have paid tax.

“Deductions are only available if you actually spend money,” says Vincent Scali, a partner at tax adviser Nexia Sydney. “People are so concerned with getting deductions into their tax return, but they don’t think about the fact that means you need to spend the money.”

“It’s not always about just chasing the deduction. It’s thinking practically – where is my money best spent right now?”

For some people, that will mean superannuation.

Super contribution tax deductions explained

The first deduction is to top up any shortfall between the concessional contribution cap and the concessional contributions you put into your super account in the year.

This is by far the easiest way for most people to get a large tax refund, but for reasons we will look at later, many high earners choose not to top up with super, says Chris Balalovski, partner at tax adviser BDO.

Concessional contributions include the mandatory 12 per cent super guarantee paid by your employer (SG contributions) and any “salary sacrifice” contributions you make to super via your weekly or fortnightly pay.

If there is any space between the cap – currently $30,000 but rising to $32,500 on July 1 – and what went into your super you can top your super up to that cap and claim a tax deduction for the contribution.

And you can backdate those missed contributions over five years, provided you are 66 or under and have less than $500,000 in super.

“It’s a two-prong tax-effective strategy – there’s the immediate tax deduction, whereby you’re reducing your taxable income, and you are also getting capital into that 15 per cent tax environment in super,” says Christine Atencia, a partner at Nexia Sydney.

In Suganthi’s case, the super guarantee contribution from her taxable income of $220,000 is $26,400, meaning there is a gap of $3600 that she can contribute from her after-tax income this year. That amount would be tax deductible.

Analysis of the table above, provided by Adrian Raftery, the author of 101 Ways to Reduce Your Tax – Legally, shows that if Suganthti had contributed nothing extra to her super over the previous four years as her salary grew at 4 per cent a year from $200,000 to $220,000, her super gap adds up to $31,700.

These calculations account for the lower concessional contribution caps that applied in previous years and previously lower super guarantee rates.

If she contributes $31,700 to her super she not only adds to her retirement savings but gets a tax deduction equal to that amount.

As the table shows, the potential deduction is bigger for Jan because the gap between the concessional cap limit and her SG contributions is greater. Her allowable deductions add up to $76,850.

Even more powerful for the self-employed

For Martin, the deduction could be even larger because Raftery says many self-employed people fail to pay themselves any super contributions.

“For the majority of sole traders, superannuation is one of the last things that they think of because it’s all about the ABC of their business – absolute bloody cash flow. The last thing they look at is paying super to themselves because they need to worry about the materials for the next job,” Raftery says.

But when the self-employed get a bit of spare cash, it can make sense for them to contribute a big whack to super, especially as they will also get a cheque from the Tax Office for close to half of their contribution if they are on the top marginal tax rate, Raftery says.

Martin could contribute up to $167,500 under the super five-year catch-up rule if he hadn’t previously put anything into super.

The biggest reason Balalovski’s high-net-worth clients don’t take up the opportunity for generous super tax deductions is because super is locked up until retirement, and they fear that the rules around it could change.

“My clients typically say: ‘I’m not interested’,” says Balalovski. “The tax deduction is just simply not worth it. They say: ‘I don’t care because it’s locked away, I won’t get the same tax deduction in my pocket that I have to spend, so there’s more locked up than I get back in a cheque from the Tax Office’,” he says.

Nexia’s Atencia says people often need the money to pay for things in their life now – such as a mortgage – rather than saving it for their retirement.

“But if you’re looking purely at the numbers point of view, it does tend to make sense,” Atencia says.

Prepay interest on investment loans

Anyone with an investment loan for a property or shares can prepay the interest on that loan that would be due in the next financial year. That allows them to bring forward the tax deduction.

In this case, let’s assume Martin, Suganthi and Jan all have a loan with a balance outstanding of $716,711 – that was the national average size of investment loans in the December quarter, according to the Australian Bureau of Statistics.

Assuming their interest on that loan is 6.21 per cent – the average nationally on investment loans, according to the Reserve Bank – that amounts to an annual interest bill of slightly over $45,000.

If they had the money available, all three could prepay next financial year’s interest before June 30 and claim a tax deduction for it this financial year. However, if they do this, they won’t be able to claim a tax deduction for investment loan interest the following year.

This deduction is much more normal for Balalovski’s clients, and it is particularly beneficial if you think you will have a higher taxable income this year than next financial year, he says.

Scali says his clients also use this strategy, especially if they have a big capital gain in one particular year that they are looking to offset.

Car expenses logbook

You can’t claim your commute to work, but sole traders and employees can claim a tax deduction for the proportion of private car use for work trips, or to travel from one workplace to another.

If you travel up to 5000 kilometres a year, you can claim 88¢ a kilometre. You don’t need to keep a logbook, but you will have to be able to show how you calculated that amount. That amounts to a tax deduction of $4400.

But if you keep a logbook for 12 weeks to work out how much of the time your car is used for work, you can also claim a percentage of the running costs (fuel, registration, insurance) and depreciation. The logbook has to contain the kilometres travelled, with odometer readings, dates and the purpose of travel.

“Historically, the logbook method results in a greater deduction. The trade-off is that there’s more effort involved because you’ve got to maintain the logbook for the representative period.

“Then you’ve got to keep all of the expenditure records, oil, fuel, tyres, maintenance, repairs, registration and that can be challenging for some people,” Balalovski says.

If you travel more than 5000 kilometres for work a year, the logbook method is far superior, Raftery says, and there is no upper limit on the amount you can claim.

Salespeople can clock up significantly more work travel, with BudgetDirect estimating they can travel 20,000 to 50,000 kilometres a year for work. Taking into account the current high fuel prices, Raftery says this could add up to total deductions of $18,000 a year or more.

And if you are driving a new car, the sharp rate of depreciation on a new vehicle (new cars typically lose 20 per cent to 25 per cent of their value in the first year of ownership, according to Canstar), means this alone can make it worthwhile to use a logbook – at least in the first year of ownership.

Say Martin, Jan or Suganthi bought a car worth $50,000 and drove it for work 35 per cent of the time – so they travelled 5000 kilometres for work out of a total of 14,300 kilometres.

At 25 per cent, the depreciation on a $50,000 car would be $12,500 in the first year, so they would be able to claim about $4400 in depreciation alone – the same level as the entire deduction allowed under the cents per kilometre method.

As the value of the motor vehicle rises, Balalovski says the advantages of the logbook method increase.

Instant asset write-off

Martin, as a sole trader with a turnover of less than $10 million, also has the ability to instantly cut his tax bill by $20,000 thanks to the instant asset write-off which is for eligible assets that cost less than $20,000.

To be eligible, assets must have been first used or installed ready for use between July 1, 2025 and 30 June 30, 2026.

The $20,000 limit also applies on a per asset basis, so you can instantly write off multiple assets.

Eligible assets include things such as computers, vehicles, office equipment (including coffee machines), freestanding office furniture and tools.

This deduction is especially useful for sole traders because any deduction they make comes off their personal tax, Raftery says.

Pay-as-you-go wage earners can also claim deductions for many assets, but they have to stick to depreciation schedules, they can’t claim the write-off instantly, he says.

If Martin, or you, claim this deduction, it is important to make sure you quarantine the asset as much as possible for business use, Balalovski says.

That can be hard if you are a sole trader. A computer that you claim a deduction must be used by the business – it should have no personal use, he says.

Having said that, if you buy an ergonomic chair for your home office and occasionally sit in it when not working, the Tax Office is unlikely to have an issue.

“From experience I know that minor, infrequent, and incidental personal use is not going to cause a problem,” he says.

Insurance, conferences, donations

Another deduction that many taxpayers fail to consider is income protection insurance, says Nexia’s Atencia.

Unlike life insurance, income protection premiums are fully tax deductable and if you are older the cost of this insurance – which pays you an income if you become unable to work – can be significant.

For example, annual premiums paid personally for a 35-year-old to ensure they received an income of $12,833 a month until age 65 should they be unable to work would be about $1620 for a man or $2520 for a woman Nexia calculations show.

For Martin, assuming he was 50, his annual premium would be $3780 – a little higher than an employee.

Both employee taxpayers and sole traders also have the opportunity to claim back the costs of attending conferences or other work-related travel before June 30, but Balalovski says it is important not to claim a deduction for costs added on to a conference, such as family holiday.

“The tax commissioner has issued some really detailed guidelines, and if you’re after a rule of thumb, one that seems to make the most sense for a lot of people is the number of days,” he says.

“If the number of days is private purposes 50 per cent and 50 per cent for business, then perhaps 50 per cent of the entire expenditure would be deductible.”

Lastly, anyone can also claim a depreciation for charitable donations – or donations to groups such as political parties.